One of the most common things I hear from retirees is this:

“I’d rather keep my money invested. The annuity company is just giving me my own money back.”

I get it. I really do. But what if that belief is actually causing you to spend hundreds of thousands of dollars less than you safely could in retirement?

Let me show you what I mean.

How Most People Think About Retirement Income

Most people think about retirement like this:

“I have a pile of money. I’ll live off the interest. Maybe I’ll spend a little of the principal here and there.”

This is called a Systematic Withdrawal Plan, or SWP. And on the surface, it makes sense. But it comes with some serious risks that most people don’t think about until it’s too late.

Here are the big ones:

- Sequence of Returns Risk — the order in which you receive gains or losses matters enormously

- Longevity Risk — outliving your money (the #1 fear retirees have)

- Withdrawal Rate Risk — spending too much too soon

- Behavioral Risk — panic selling when markets get choppy

Income annuities can protect against all of these. But today, I want to focus on the two biggest ones: sequence of returns risk and withdrawal rate risk.

The Order of Returns Matters More Than You Think

Here’s something most people forget: the order in which you receive your investment returns matters just as much as the returns themselves.

Think about 2008. Think about 2022. Think about 2000, 2001, and 2002. Those were real events. And people who retired in those years got off to a very bad start.

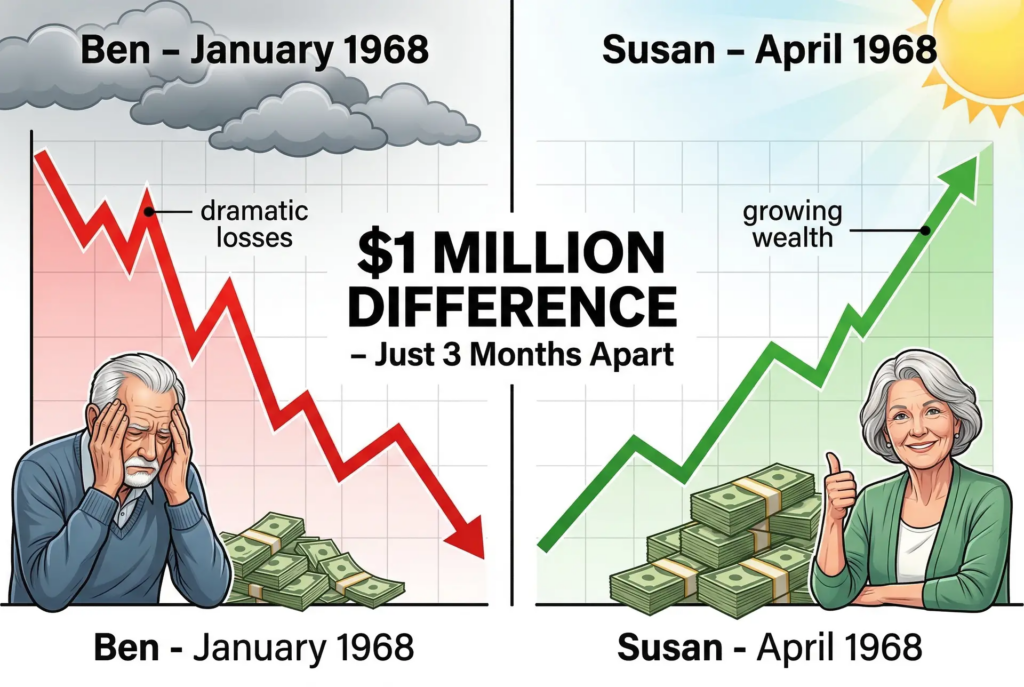

Here’s a real example that drives this home.

Two people retired just three months apart — one in January 1968, one in April 1968. Same starting amount. Same withdrawal strategy. By the end of their retirement, the person who retired in January ended up with almost $1,000,000 less than the person who retired just three months later.

Three months. One million dollars. That’s how powerful — and how dangerous — sequence of returns risk is.

And here’s the thing: our markets today are even more volatile than they were in the 1960s or early 2000s. High frequency trading and market algorithms have made swings faster and sharper. This risk is not going away.

The 4% Rule Is a Speed Limit on Your Money

Now let’s talk about withdrawal rate risk.

You’ve probably heard of the 4% rule. It was originally written about by William Bengen in the early 1990s, and it’s still widely referenced today. The idea is simple: if you withdraw 4% of your portfolio per year, your money should last through retirement.

For a $1,000,000 portfolio, that’s $40,000 per year.

But here’s what most people don’t realize about the 4% rule:

It’s not designed to maximize your spending. It’s designed to prevent disaster.

It’s basically a speed limit placed on your own money. Even if the markets perform well. Even if you don’t live to 95. You still have to obey that speed limit — because you don’t know what’s coming around the next curve.

Think of it this way. You want to get on the Autobahn. But instead, you’re stuck on a back road doing 40 miles per hour. That’s what the 4% rule feels like when markets are actually doing well.

And even at that cautious pace, it’s still not foolproof.

What Income Annuities Actually Do

Here’s where income annuities change the math entirely.

Instead of one person trying to plan for every possible lifespan, thousands of retirees share that risk together. This is called risk pooling.

Insurance companies know that some people will receive income for 10 years. Others will receive it for 30 years or more. The pool balances out. And because of that balance, the income that can be paid out is almost always higher than what a cautious withdrawal rate would allow.

So is the annuity just giving you your own money back?

At first — yes. But here’s what most people miss: because of risk pooling, you’re getting it back at a much higher rate than you could ever safely withdraw from a managed portfolio. And it’s guaranteed for as long as you’re alive. As long as you have a heartbeat, it pays.

Let’s Look at the Numbers

Let’s use a simple example. A 65-year-old couple with $500,000 to work with.

| Systematic Withdrawal Plan | Income Annuity | |

|---|---|---|

| Annual Income | $20,000/year (4%) | $37,000+/year |

| Guaranteed? | No | Yes |

| Market Risk? | Yes | No |

| Longevity Risk? | Yes | No |

That’s 86% more spendable income — guaranteed — with no market risk and no risk of running out.

Now here’s the question worth asking: what return would a money manager need to earn on that same $500,000 — after fees of 1.5% — to match that $37,000/year income and make sure it lasts to age 95?

8.6% every single year. With no down years. Ever.

The next time someone tells you “you can do better in the market,” ask them to sign a document guaranteeing that return. Watch them go quiet.

What About Inflation?

This is a fair concern. Let’s look at it honestly.

With the managed portfolio, starting at $20,000/year and taking a 3% inflation increase each year — it would take 22 years just to reach the same $37,000/year the annuity was paying on day one.

Here’s how the total spendable income compares after 22 years:

| Total Income After 22 Years | |

|---|---|

| Systematic Withdrawal Plan | $610,000 |

| Income Annuity | $818,000 |

| Difference | $208,000 |

And remember — the $610,000 from the portfolio isn’t guaranteed. The $818,000 from the annuity is.

Let’s stretch it out to 30 years:

| Total Income After 30 Years | |

|---|---|

| Systematic Withdrawal Plan | $950,000 |

| Income Annuity | $1,100,000+ |

The gap narrows over time — but the longer you live with a managed portfolio, the more all those risks compound. Longevity risk. Inflation risk. Sequence of returns risk. They all pile up together.

The Real Question to Ask

The real question isn’t whether income annuities are perfect. They’re not. Nothing is.

The real question is this:

How do you create reliable income for the rest of your life without taking unnecessary risk?

When the paychecks stop — from your job or your business — everything changes. Market volatility matters more. Sequence of returns risk matters more. Longevity risk becomes very real.

That’s why income annuities exist. Not to replace investing. To replace paychecks.

When used correctly, they’re not competing with your portfolio. They’re stabilizing it.

Because the biggest financial mistake in retirement isn’t earning too little.

It’s running out.

Is an Income Annuity Right for You?

If you’re within 5 to 10 years of retirement — or you’re already retired — and you’ve accumulated anywhere from a few hundred thousand to several million dollars, it may be worth having a real conversation about how to turn that into reliable income.

I offer a Retirement Income Clarity Call — a short, structured Zoom conversation where we look at your assets, your income goals, and determine whether an income annuity actually makes sense for your situation. If it’s not the right fit, I’ll tell you that clearly.

You can book directly on my calendar here.

All the best,

Marty Becker

Podcast Episode 105: Do Income Annuities Just Return Your Money Back To You?

Download Episode 105: Do Income Annuities Just Return Your Money Back To You? on Apple Podcast