AI can do a lot of things.

It can write essays. It can crunch numbers. It can answer almost any question you ask it.

So it makes sense that people are now asking AI about their retirement money.

But here’s the truth about AI annuity advice —

It can help you. But it can also hurt you.

And in retirement, the difference between the two can cost you a lot.

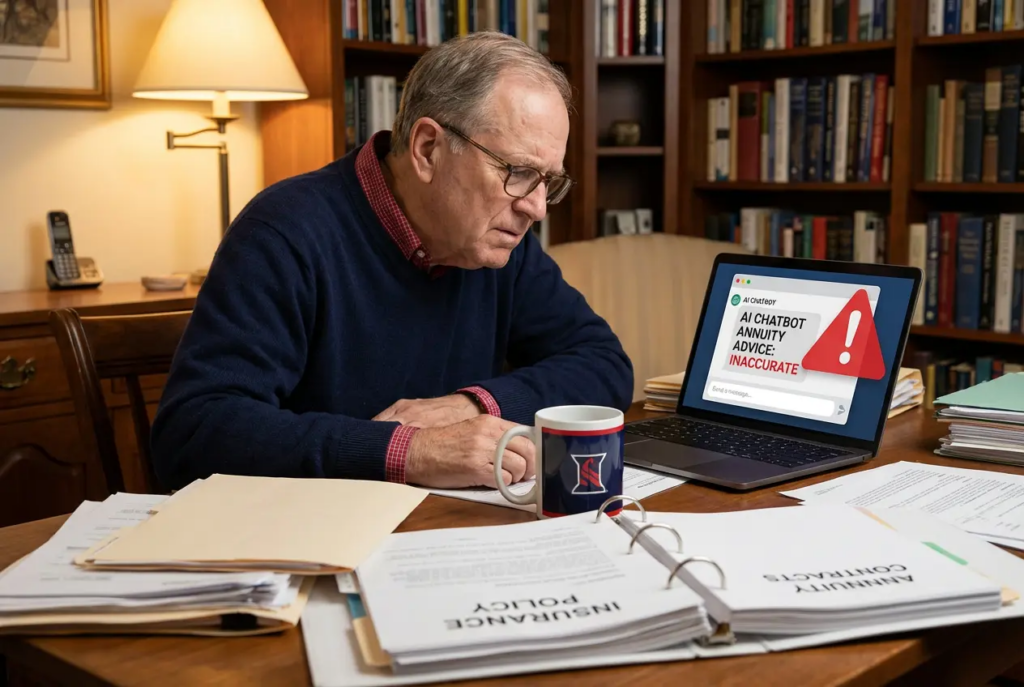

It Already Happened to One of My Clients

A client called me not long ago wanting a specific annuity.

I asked why that one.

“AI said it was the best one.”

The problem?

That product wasn’t even available in their state.

That phone call is exactly why I’m writing this today.

So I Asked AI Myself

I went straight to the source and asked AI three questions:

- When does it make sense to use AI annuity advice?

- When does it NOT make sense?

- How will AI change the annuity industry in the future?

Here’s what I found.

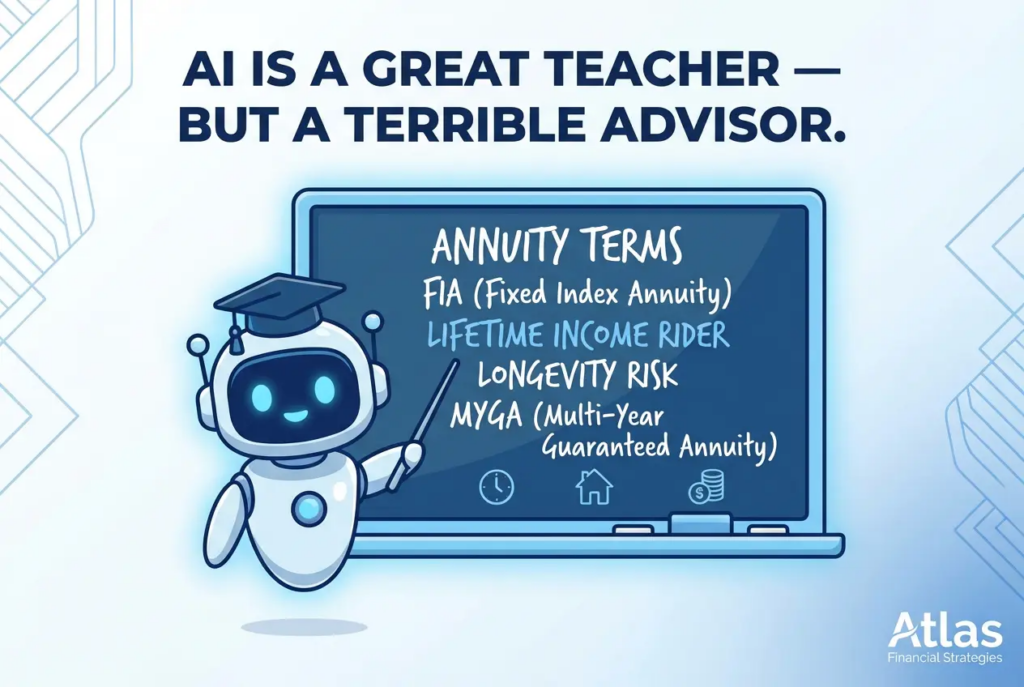

When AI Annuity Advice Actually Works

Good news first.

AI is a great tool for learning about annuities.

You can ask it:

- What is an FIA?

- What is a MYGA?

- What is a lifetime income rider?

- What is longevity risk?

And most of the time you’ll get a pretty accurate answer.

Honestly, AI annuity advice can explain complicated financial concepts in plain English better than most insurance company brochures.

If you’re trying to learn the language of retirement income planning — AI is a great place to start.

When AI Annuity Advice Becomes a Costly Mistake

Here’s where it goes wrong.

The trouble starts when people stop learning and start asking:

- “Which annuity should I buy?”

- “Should I put my retirement savings into an annuity?”

That’s the moment AI annuity advice crosses from education into personal advice.

And that’s the moment it can cost you.

Here’s Why

Annuities are not one product.

There are thousands of annuity products from hundreds of different insurance companies.

Every single one is different:

| What Varies | Why It Matters |

|---|---|

| Income riders | Determines how much you get paid |

| Payout factors | Affects your monthly income amount |

| Crediting strategies | How your money grows |

| Liquidity provisions | When and how you can access your money |

| Tax situations | How it affects your overall retirement plan |

| State availability | Not every product is available everywhere |

The right annuity depends entirely on your personal situation.

AI doesn’t know your age. Your health. Your income needs. Your tax situation. Or what products are even available where you live.

That’s not a small gap. That’s a canyon.

The Simple Rule for AI Annuity Advice

Here’s how to think about it:

Use AI Annuity Advice For This Use AI Annuity Advice For This |  Don’t Use AI Annuity Advice For This Don’t Use AI Annuity Advice For This |

|---|---|

| Learning annuity terms | Choosing a specific annuity |

| Understanding how annuities work | Deciding how much money to put in |

| Researching general concepts | Comparing products for your situation |

| Preparing questions for your advisor | Replacing your advisor |

AI is a great starting point.

It is a terrible finish line.

The Bottom Line

AI annuity advice is a powerful learning tool.

But when it comes to choosing the right annuity for your retirement — there is no algorithm that knows your life better than a real conversation with someone who does this every single day.

You’ve spent decades building your money.

The stakes are too high for incomplete information.

Don’t let a chatbot make one of the most important financial decisions of your life.

Podcast Episode 106: AI Annuity Advice: Don’t Make This Costly Mistake

Download Episode 106: AI Annuity Advice: Don’t Make This Costly Mistake on Apple Podcast