Most people think retirement planning is all about money. They focus on their 401k, Social Security timing, and interest rates. But there’s another kind of retirement that nobody talks about. It’s the psychological retirement. And if you don’t prepare for that one, the money won’t fix it.

Today, I want to walk through what actually happens inside your mind when you leave a lifelong career. Then we’ll talk about how financial structure can help stabilize that transition.

Retirement Is More Than One Day

Retirement is more of a process than just a single event. Research shows that retirement is actually a multi-year psychological transition, not just a single moment.

Most people expect permanent freedom. But many retirees experience this in phases, almost like marriage.

The Four Phases of Retirement

Phase 1: The Honeymoon Phase

At first, retirement is nice. You don’t have to get up early. You don’t have to be anywhere at a certain time.

Phase 2: Disenchantment

Then you start to become bored and a little restless.

Phase 3: Uncertainty

A lot of uncertainty sets in about what you’re going to do every day.

Phase 4: Reorientation and Stabilization

People can start to reorient if they want and rebuild an identity that’s separate from their career. Eventually, with work, they can find stabilization.

Why Does This Happen?

Work provided more than just income. It provided:

-

- Structure

-

- Social contact

-

- Status

-

- Immediate feedback on what you’re doing

-

- A sense of mattering

When that disappears, your brain has to recalibrate to this new lifestyle. And that recalibration can really start to feel unsettling over time.

The Identity Shock

One of the strongest themes in retirement is identity loss.

When someone asks you, “Hey, what do you do?” your answer is, “Well, I’m retired.” And there’s really not a whole lot to say after that initial answer because you don’t have a clear answer anymore.

That can actually hit harder than most people expect. This is especially true if you were:

-

- A high achieving professional

-

- A business owner

-

- A first responder

-

- A police officer

-

- A fireman

-

- In the military for 20, 25, 30 years

-

- A high level executive

A lot of those people really identify with those roles they’ve lived for two, three, four decades.

This is where anxiety can really start to creep in for people. And it has nothing to do with finances. It’s not because they’re broke. It’s really just because now they’re untethered. They have no direction.

The Mattering Problem

Research highlights a lot about just mattering. The sense that you are making a difference in your everyday life.

Your work and your career constantly reinforced that you mattered:

-

- Someone needed you on a day-to-day basis

-

- An organization depended on you

-

- You were probably contributing to something larger than yourself

Retirement removes that feedback loop literally overnight. You wake up one day, and you don’t have anywhere to be.

When people feel less useful, that’s when depression can start to sink in. This is particularly true if retirement was involuntary or unplanned.

I’ve been getting a lot of phone calls about that. People are being forced into retirement. They didn’t plan on retiring, but they were forced out. That unplanned retirement didn’t really give them a whole lot of time to mentally prepare for this major shift.

The Loneliness Risk

Work for a lot of people is a built-in social system. A lot of people hang out with people that they work with because they’ve known them for decades.

Once that disappears, contact with others can drop off dramatically.

Research shows that loneliness risk varies by context. But involuntary retirees often report the highest levels of isolation. They had work friends one day. Then those friends just disappeared.

Loneliness is not just emotional discomfort. It is strongly associated with mental health decline.

Psychological Solutions

Before we talk about money, let’s talk about some psychological solutions for anyone who may be dealing with this shift and struggling with it.

The good news is that the research is very clear about what helps people who are struggling with retirement.

Solution 1: Build Replacement Roles

You want to build some replacement roles intentionally. Don’t just see what happens after you retire.

If you’re not retired yet, define two or three roles before you actually get to that threshold. This is going to help you immensely.

If you’re already retired and you’re not doing something like this, I would strongly consider it.

Ideas for replacement roles:

-

- Become a mentor

-

- Volunteer as a leader of an organization

-

- Become a coach

-

- If you attend church, look into becoming a contributor (I know a guy who just works the parking lot because he can talk with people as they’re pulling in)

-

- Become a board member for a charity or an organization (certain credit unions are always looking for people to volunteer as a board member)

-

- Go back to school or learn a new skill

-

- Become a caregiver by choice (help elderly neighbors, cut their grass, rake their leaves, check in on them, drive them to a doctor’s appointment or the grocery store)

These roles with a visible contribution actually can help rebuild your identity.

Solution 2: Structure Your Days

Freedom without structure just really turns into drift.

When you’re new and you’re in this honeymoon phase, it’s nice to sleep in and not have to get up and be anywhere. But after a while, staying in bed too long can actually fuel depression.

Ways to add structure:

-

- Establish a fixed wakeup time

-

- Join a gym or some sort of exercise club

-

- Add cognitive activity to keep yourself stimulated (not just sitting around watching cable news)

-

- Sign up for some classes

-

- Dig deep into a subject you’ve always been interested in but never really had the time to learn about

-

- Maybe even teach a class somewhere

-

- Sign up for some social commitments where you have to be somewhere, and people are counting on you showing up

Sleep and fatigue often improve after retirement. Yeah, it’s nice to sleep in. But they only improve when structure replaces the work anchors.

If you don’t like getting up early, schedule stuff at 10:00 a.m. Plenty of time to sleep in. Or whatever works for you. But have some sort of schedule almost on a daily basis.

Solution 3: Multiply Your Social Memberships

Research consistently shows that retirees with multiple group memberships have better outcomes.

Not just friends, but groups like:

-

- Men’s and women’s groups, like the Elks (a great organization that does a lot of volunteer work)

-

- A golf club

-

- A fitness group

-

- A church group

-

- If you’re a numbers guy, maybe an investment club where people get together, throw a little money in the pot, decide on what they want to invest in, and then split the profits

-

- If you’re someone who has a lot of experience in a certain area, maybe look at mentoring

The more identity anchors that you have, the better off you will be in the long term.

Solution 4: Be On Guard for Financial Strain

This is where the psychology and the money begin to intersect.

Research shows that subjective financial strain (everything in your head and how insecure you feel about it) predicts anxiety and depressive symptoms more strongly than your objective wealth alone.

What does that actually mean? That means you can actually have enough money and still feel unsafe. And that feeling matters.

The Financial Transition: From Paycheck to Portfolio Shock

For 30 to 40 years, the money flowed in predictably. Then suddenly, you have to withdraw from your assets. The brain experiences this as a loss, even if it’s mathematically sound.

Then you add in a little mix of:

-

- Market volatility

-

- Inflation headlines

-

- Sequence of returns risk

That is psychologically powerful because it creates the fear of “what if my timing is off.”

That perceived loss actually fuels more anxiety, and it becomes a vicious cycle.

How Annuities Help With the Psychological Transition

This is where annuities come into play and can help with this particular area of the retirement struggle.

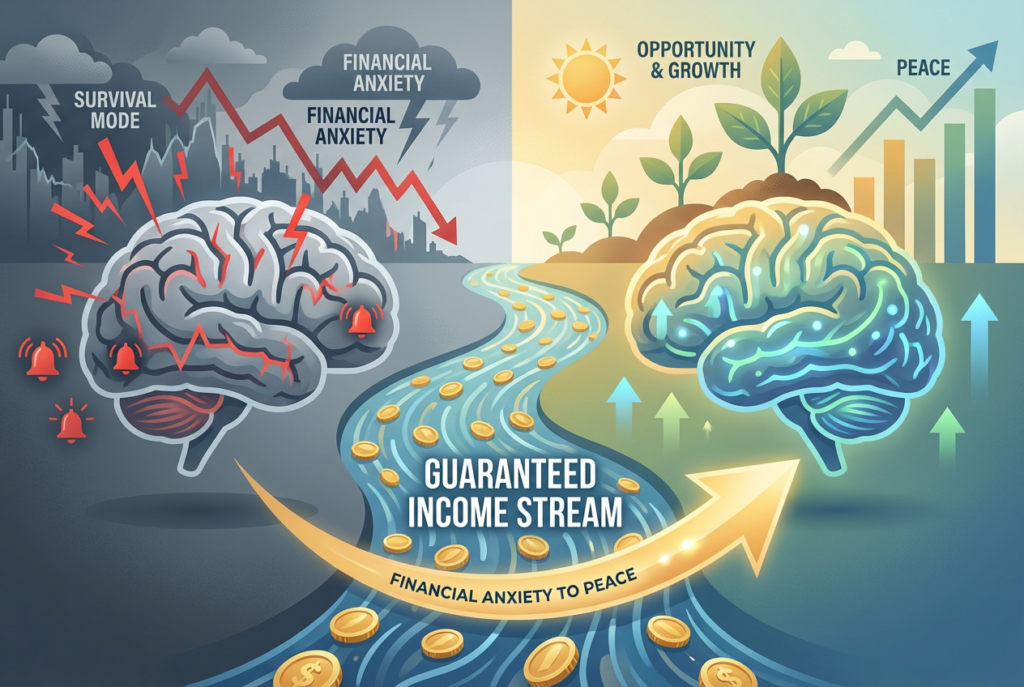

Annuities aren’t just a financial product. They help recreate predictability.

Income Stability Changes the Brain

When your essential expenses are covered by a guaranteed income (annuities, pensions, Social Security), the vigilance that you’re constantly implementing decreases.

Your brain is actually designed to be a threat-seeking machine. Just really sit and think about that. Think about when you’re walking through the yard, and you don’t put the garden hose away. Your brain sees that as a snake, and it startles you. It’s constantly thinking about threats.

That vigilance can be exhausting.

What decreases when you have a guaranteed income:

-

- Balance checking decreases (I’ve had a lot of clients tell me, “Hey, I just don’t want to feel like I have to look at the market every day”)

-

- Catastrophic thinking decreases (this is what’s known as an amygdala hijack – the amygdala is the fear center of your brain, and it can actually overreact and start to catastrophize everything in your life)

When you have essentials covered, it calms that fear center of your brain.

What improves:

-

- Marital tensions decrease (maybe the wife wants to go out to dinner more, wants to travel more, or socialize more, and the man’s thinking, “Well, there’s 150 bucks to go to dinner.” You can just put all that aside, knowing that the money is going to show up again next month, just like throughout your working career.)

-

- Perceived control actually increases

-

- Calm and peace increase

-

- Life satisfaction increases

Annuities as Psychological Infrastructure

Think of them as retirement scaffolding. Those big things that they build up so the guys can walk back and forth doing brickwork or siding.

Annuities don’t eliminate market risk. They eliminate your personal survival risk.

When housing, food, utilities, insurance, and basic living costs are guaranteed, the growth portfolio becomes opportunity capital, not survival capital.

Think about that psychological shift.

That shift alone can:

-

- Reduce hopelessness tied to your personal financial security

-

- Encourage purposeful spending

-

- Support identity rebuilding (knowing that you don’t have to sit in front of your computer or watch CNBC all day – you can actually go do something to help contribute to the rebuilding of your identity)

-

- Reduce panic selling during downturns (because you can survive the ups and downs of the market when all of your essential spending needs are already in place on a guaranteed basis)

It’s Not About IRR

The other psychological shift that needs to take place is that people have to realize and accept that this is not about IRR or ROI anymore.

Stan the Annuity Man has a good saying: “You don’t know your ROI until you die.”

The deeper question is: If guaranteed income allows someone to:

-

- Sleep better

-

- Spend more confidently

-

- Actually engage socially and enjoy it

-

- Avoid fear-based decisions

-

- Help protect their marriage by being able to go and do things and enjoy themselves

-

- Feel secure in your aging (because all these other problems actually multiply with longevity)

Honestly, what is that really worth?

Retirement success isn’t just a Monte Carlo score. It’s emotional stability and peace of mind in retirement. And peace of mind comes from predictability.

The Real Question

At the end of the day, retirement isn’t about who you were and what you did through your career. It’s really about who you will become in this next phase of your life.

Yes, money matters. You can’t do anything without money. But money without emotional stability cannot create peace.

The question isn’t just “will my portfolio last.” It’s “Will I feel secure enough to really enjoy this stage of my life?”

Because when income is predictable, your identity can expand. You can take the focus off one thing and put it into something else that’s honestly more important.

When the fear is reduced, that’s when freedom grows. Mental, emotional, spiritual freedom.

And that’s what a real retirement strategy should deliver.

Next Steps

If you do not have a retirement strategy that implements predictable income, then it’s time to talk.

The best way to see if the Atlas Annuity Strategy will work for you and your personal situation is to book a short Retirement Income Clarity Call with me by clicking here.

Podcast Episode 104: Retirement Planning: The Psychological Transition Nobody Prepares For

Download Episode 104: Retirement Planning: The Psychological Transition Nobody Prepares For on Apple Podcast