If you’ve ever wondered why retirement feels more complicated than it should, you’re not imagining things. For decades, people were told to save enough, invest wisely, and then withdraw 4% every year. But new research from Morningstar tells a very different story—one that explains why so many retirees feel uneasy and why guaranteed income tools like annuities are becoming more relevant than ever.

Morningstar’s 2026 Research On Retirement Income

Morningstar just released their “State of Retirement Income 2025” report (released December 3rd, 2025), and the numbers are eye-opening. For someone retiring in 2026, the highest safe withdrawal rate for a stable, inflation-adjusted paycheck over 30 years is 3.9%.

That means if you have a $1 million portfolio, you can safely withdraw about $39,000 per year. And here’s the kicker—that still has a 10% chance of failure.

This is what Morningstar calls their “base case.” Now, before you jump into the comments saying “Well, my guy says I can take 6%”—totally fine. You do you. Morningstar does acknowledge that some flexible strategies support withdrawal rates as high as 5.7% (or $57,000 per million). But here’s the tradeoff:

-

- Income becomes more volatile

-

- Spending cuts are required in bad markets

-

- Outcomes vary more widely

In other words: more income upfront equals less certainty.

The Real Killer: Sequence of Returns Risk

Here’s what most people don’t understand about the 4% rule for 2026. The problem isn’t that markets stay bad forever. The problem is what happens early in retirement.

Think of retirement like crossing a river. The average water depth doesn’t matter. What matters is that the stone is above water when you take your first step. That’s the sequence of returns risk in a nutshell.

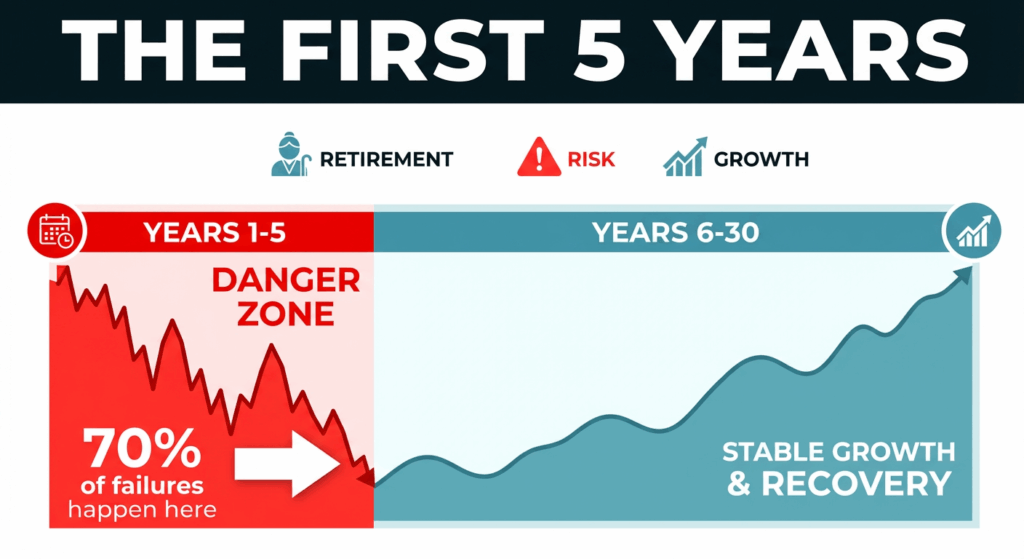

Morningstar found something shocking: Of the retirement plans that failed, nearly 70% failed because they experienced losses in the first 5 years.

Once income starts coming out of a shrinking portfolio, the damage compounds over decades. You can’t recover from those early losses because you’re taking money out at the worst possible time.

This is why retirees don’t need more return. They need less stress on the portfolio, especially in the early years.

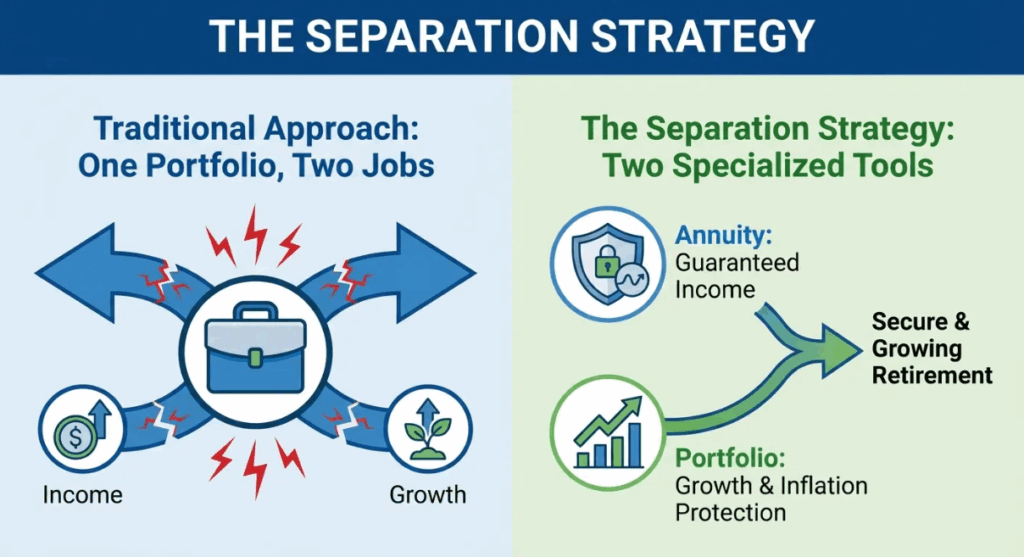

How Guaranteed Income Changes Everything

This is where the conversation shifts. Morningstar’s research shows that adding non-market-based income—things like Social Security, defined benefit pensions, or guaranteed income annuities—dramatically stabilizes retirement outcomes.

Think of your retirement plan like a house:

-

- Your portfolio acts as the walls

-

- Guaranteed income is the foundation

As long as the foundation is solid, the walls don’t have to carry the full weight of the house.

Now, I’m not saying annuities are designed to outperform markets. That’s like comparing an F-250 to a Corvette. The Corvette isn’t designed to drive through 8 inches of snow—it’s designed to look flashy and get you there faster. Two totally different vehicles.

Annuities are designed to remove pressure from your other investments, especially in the years when pressure is most dangerous.

“But What About Inflation?”

This is always the first objection, and it’s a fair one. People hear “level income” and think, “Won’t inflation destroy this plan over time?”

Morningstar actually gives us the framework to answer this. Yes, inflation-adjusted annuities exist. I have access to them. But they come with a major tradeoff: much lower starting income. In fact, I’ve never sold one because when someone sees the starting income, it’s a total turnoff.

But here’s the reality most retirees don’t consider: Inflation risk hurts most in the early years, not the later ones.

Morningstar’s research shows that inflation early in retirement is far more damaging than inflation later on because those costs compound over decades. For people who retired in 2020, 2021, and 2022—when there was a market dip AND rapid inflation—irreversible damage could have been done to traditional portfolio-based retirement plans.

So the question becomes: Would you rather start with too little income today, or enough income now with flexibility later?

Here’s How It Works:

Level payment annuities solve the most dangerous retirement risks right out of the gate:

-

- ✓ Sequence of returns risk

-

- ✓ Market volatility

-

- ✓ Income gaps in the early years

And Morningstar shows that stable income sources allow portfolios to better absorb inflation shocks because you’re not forced to sell investments at the wrong time.

Think of it this way:

-

- An inflation-adjusted annuity is like buying a coat that gets thicker every year, but starts out too thin to keep you warm today

-

- A level annuity is a warm coat right now, and you can add layers down the road if needed

What the Annuity Provides:

-

- Covers baseline income needs (your bills, your survival expenses)

-

- Buys you time and flexibility so you’re not panicking and selling at the wrong time

-

- Allows growth assets to address inflation dynamically over time

Inflation isn’t ignored—it’s assigned to the right tool, which is equities. Stocks are the best long-term solution for inflation.

The Longevity Factor

Morningstar highlights this repeatedly: Portfolios don’t know how long you’re going to live. Insurance companies do.

By covering essential expenses with guaranteed income:

-

- Market downturns matter less

-

- Spending adjustments are smaller

-

- Inflation becomes a manageable variable, not a crisis

Here’s a subtle but important point: Most retirees don’t spend more every single year. Most financial planning software (including mine) shows a 2-4% inflation increase every year for the rest of your life. But that’s not reality.

Morningstar confirms that real-world spending often declines later in retirement. Starting with strong income early—when you’re still healthy, mobile, and active—actually aligns better with reality than backloading income growth that may never be fully used.

Two Strategies Compared: Portfolio-Only vs. Atlas Annuity Strategy

Let me show you two different approaches to a $1 million retirement portfolio.

Option A: Portfolio-Only Withdrawal (Morningstar Base Case)

Starting Portfolio: $1,000,000

Withdrawal Rate: 3.9%

Annual Income: $39,000

Key Characteristics:

-

- Income depends entirely on markets

-

- Subject to sequence of returns risk

-

- Requires careful monitoring and spending discipline

-

- Portfolio must survive 30+ years of withdrawals

-

- 10% failure rate

What’s Really Happening:

You’re asking all $1 million to do two jobs at once: produce income AND survive market volatility long enough to keep paying that income.

Option B: The Atlas Annuity Strategy + Portfolio

For a typical 65-year-old couple, here’s how we structure it:

Annuity Allocation: $516,000 (split into two annuities)

Guaranteed Annual Income: $39,000 for life

Remaining Portfolio: $484,000

Key Characteristics:

-

- Income is guaranteed and not market-dependent

-

- Sequence risk on income is totally eliminated

-

- Portfolio no longer needs to fund baseline spending

-

- Remaining assets can be invested for growth, inflation response, liquidity, and legacy

What’s Really Happening:

You’ve separated the jobs your money is performing. The annuity produces income. The portfolio absorbs volatility and addresses inflation.

Side-by-Side Comparison

| Feature | Portfolio-Only | Atlas Strategy |

| Annual Income | $39,000 | $39,000 |

| Income Guarantee | No | Yes (lifetime) |

| Failure Risk | 10% | 0% (on income) |

| Sequence Risk | High | Eliminated |

| Remaining Discretionary Liquidity | $0* | $484,000 |

| Portfolio Pressure | Extreme | Minimal |

| Inflation Strategy | Hope for returns | Aggressive growth |

*Note: While the full million is “liquid,” it’s committed to producing income.

The Liquidity Objection (And Why It’s Backwards)

Here’s what most people and most advisors don’t think through to the next level. The main objection I hear is: “The annuity is going to lock up my money.”

But let’s think about this logically.

If you have $1 million and Morningstar says 3.9% is the safe withdrawal rate, yes—that million is liquid. You can move it from investment to investment, adviser to adviser. But if that million is there to produce $39,000 per year, you can’t just go grab $150,000 to buy a boat. You’d mess up the whole income plan.

When you add the annuity strategy, you’re getting the same amount of income for fewer dollars allocated to the income need. That frees up almost half a million dollars, which is totally discretionary.

You want that money to stay invested. If it does really well in the early years, great—spend more, make a big purchase. But it’s also your safety net. If the market drops, you don’t have to panic sell, and you still have money invested for long-term inflation offset. (Always speak with a securities licensed advisor before buying or selling any securities)

What Should You Do Next?

If you’re new to annuities and have no clue what I’m talking about in this post, I’d highly recommend watching my intro series called “20% More Spendable Income in Retirement.”

If you’ve been here for a while and you’re at the point of retirement, book a short Zoom call with me. At least get your questions answered, and then we can figure out if the Atlas Annuity Strategy is the right fit for you. No pressure. Just answers.

Final Thoughts on the 4% Rule for 2026

The 4% rule isn’t dead—it’s just evolved. And the new math is harder. At 3.9%, with a 10% failure rate, you need to be smarter about how you structure your retirement income.

The research is clear:

-

- The first 5 years are the most dangerous

-

- Guaranteed income stabilizes outcomes

-

- Separating income from growth reduces stress and increases success rates

Key Takeaways: The 4% Rule for 2026

-

- ✓ Morningstar’s safe withdrawal rate for 2026 is 3.9% (down from the traditional 4%)

-

- ✓ Even at 3.9%, there’s still a 10% chance of running out of money

-

- ✓ 70% of retirement plan failures happen in the first 5 years due to sequence of returns risk

-

- ✓ Guaranteed income sources (annuities, pensions, Social Security) dramatically improve retirement success rates

-

- ✓ Separating income production from growth investing reduces portfolio stress

-

- ✓ The Atlas Annuity Strategy provides the same income with money remaining for growth and liquidity

Ready to discuss your retirement income strategy? Schedule a call with me.