Retirement isn’t about chasing returns. It’s about engineering income.

Last week, I sent out an email comparing CDs to MYGAs. Within hours, one of my clients—Dave—replied with a short message that stopped me in my tracks:

“Hi, Marty. I actually use 2-, 3-, 4-, and 5-year MYGAs and FIA policies to build an income ladder to fund my bucket for that year’s expenses. Far better than CDs or bond ladders.”

That was it. Short. Confident. Decisive.

So I wrote back and asked him to explain more. What unfolded through our email exchange is one of the clearest retirement income strategies I’ve ever seen.

Dave didn’t just build a ladder. He built a system.

The Real Problem Most Retirees Face

Let’s be honest about something.

Most retirees are not losing sleep over long-term averages. They’re losing sleep because they’re wondering:

-

- What if the market drops next year?

-

- What if bonds fall again?

-

- What if I have to sell something at the wrong time and take a loss?

-

- What if I run out of money too early?

Retirement doesn’t feel scary because of 20-year projections. It feels scary because of the next 12-24 months. What’s going to happen next year?

Dave understands this very well.

The Annuity Laddering Strategy

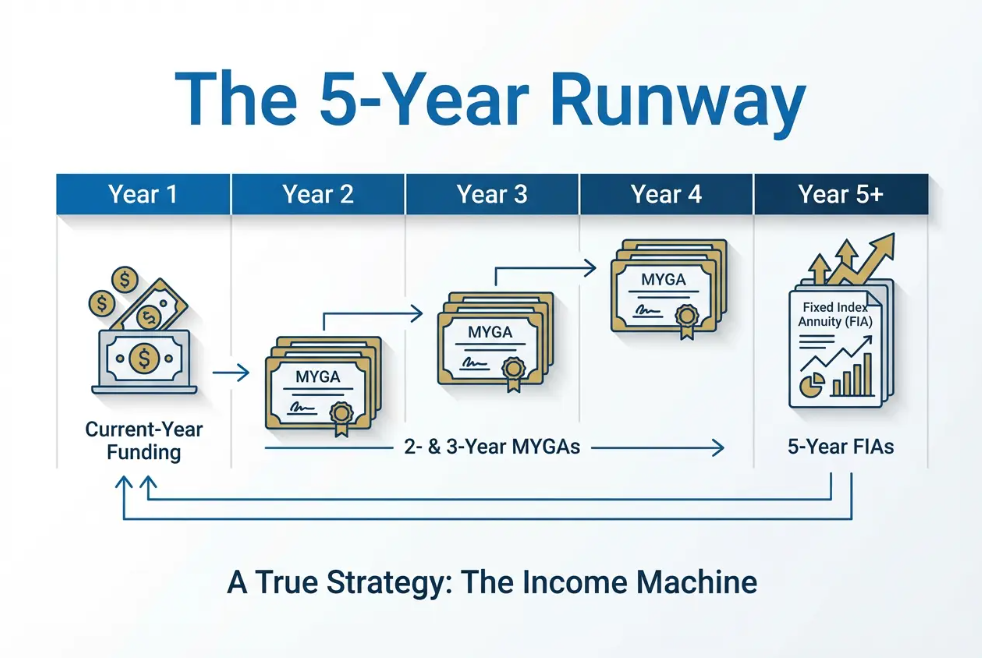

Here’s what Dave explained to me. His strategy for bucket one is 5 years of low-risk investing for immediate income.

Here’s how it breaks down:

Year-by-Year Breakdown

Year 1 (Current Year):

Money sits in a high-yield money market. This is what he’ll spend this year.

Years 2, 3, and 4:

Money is in high-yield MYGAs (Multi-Year Guaranteed Annuities).

Years 5 and Beyond:

Money is in Fixed Index Annuities (FIAs).

Let’s pause there for a second.

What Dave created was a five-year runway:

-

- Year one is fully liquid

-

- Years two through four have a guaranteed rate with a known maturity

-

- Years five and beyond are all principal-protected with growth potential

The markets can go up. The markets can go down. But Dave’s next five years? He doesn’t care.

What he really did was emotionally insulate himself against making rash or bad decisions.

Why Annuity Laddering Is Better Than CDs and Bonds

In his next email, Dave explained his reasoning. He said:

“2 to 4-year MYGAs almost always deliver higher yields than CDs and bond ladders, even higher on a risk-adjusted basis.”

Let me break down what he means.

The Problems with CDs

-

- Lower rates

-

- Annual taxation (you get a 1099-INT every year)

-

- No built-in penalty-free withdrawal structure

The Problems with Bond Ladders

-

- Interest rate risk

-

- Mark-to-market volatility (if you have to sell, you might take a loss)

-

- No built-in penalty-free withdrawal structure

-

- Annual taxation even on zero-coupon bonds

The Benefits of MYGAs

-

- Guaranteed term

-

- No daily price fluctuation

-

- Tax-deferred growth (even with non-qualified money)

-

- Higher yields in comparable durations

-

- More efficient compounding

Here’s a simple comparison:

| Feature | CDs | Bond Ladders | MYGAs |

|---|---|---|---|

| Guaranteed Rate | Yes | No | Yes |

| Tax-Deferred Growth | No | No | Yes |

| Annual Taxation | Yes | Yes | No |

| Market Volatility | No | Yes | No |

| Penalty-Free Withdrawals | Interest Only | Interest Only | Yes (10%) |

| Higher Yields | No | Depends | Yes |

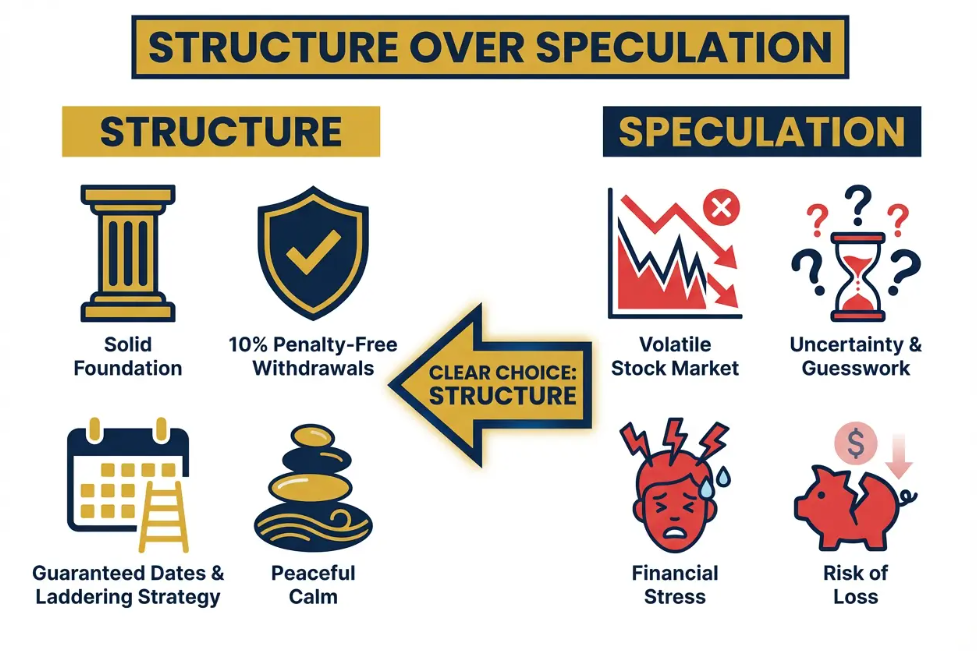

For bucket #1 money, it’s stability over speculation.

The Tax Advantage Most People Miss

Dave also pointed out something subtle that most people miss.

MYGAs actually compound internally without the annual tax drag.

With CDs and bonds (even zero-coupon bonds), you get a 1099-INT every year, whether you take the interest or not. You have to pay taxes on money you didn’t even touch.

With MYGAs:

-

- More efficient compounding

-

- More control over income timing

-

- No forced annual taxation

-

- You can defer taxes until you need to withdraw with a 1035 exchange

That tax control reduces what I call “retirement friction.”

You don’t get a tax bill while that interest is compounding. And if you get to the end of the term and you don’t need the money, you can continue to defer it.

The Flexibility Factor

One of the big objections people have with annuities is: “They’re going to lock up all my money!”

But Dave made sure his four and five-year MYGAs and his FIAs all had 10% annual penalty-free withdrawals.

Why does this matter?

Because life happens.

You could have:

-

- A medical event

-

- A family need

-

- An unexpected opportunity that requires quick cash

Bond ladders don’t offer the contractual flexibility of that. Annuity Laddering does.

It gives you breathing room. That’s really all we’re looking for here—flexibility with the option to grab some quick money if you need it.

When the Strategy Becomes a Machine

Then Dave sent his final email. And this really changed how I was thinking about this whole conversation.

He said:

“As my two and three-year MYGAs expire in 2027, I plan to replace them with 5-year FIAs until I get to the point where I just have 5-year FIAs being purchased each year and one expiring every year to feed the money market for current year funding and expenses.”

That’s when this stopped being a ladder in my mind. It became a machine.

Here’s What Happens When It’s Fully Built

Every single year:

-

- One of the five-year fixed index annuities matures

- The earnings fund the current year’s expenses (in addition to Social Security)

- A new 5-year fixed index annuity is purchased

- The cycle resets

It’s rhythmic. It’s predictable. It’s systematic.

You never have to ask: “What should I sell this year?”

You already know what’s going to mature.

That’s a big psychological difference. You don’t have to sit down and figure out:

-

- What performed?

-

- What didn’t perform?

-

- Do I need to do tax loss harvesting?

There’s a simple, predictable machine that has been built.

Removing Retirement Fragility

A few months ago, I talked about retirement fragility. What this type of annuity ladder strategy does is remove that fragility.

This isn’t only logical. It’s emotionally intelligent.

When Does Retirement Feel Fragile?

Retirement feels fragile when:

-

- Your income depends on market timing

-

- Bonds fluctuate unexpectedly

-

- You have to decide what to sell each year to fund living expenses

When Does Retirement Feel Engineered?

Retirement feels engineered when:

-

- Every contract matures on a pre-determined schedule

-

- The next year is funded automatically

-

- The following four years of money are protected and growing

Fragility in retirement creates anxiety. Structure creates calm. Structure creates confidence.

That’s what we’re going for.

Dave’s Most Important Line

Dave closed with this line, and I really appreciate it:

“Basically, whatever the market offers that fits my goals is what I will purchase.”

That’s wisdom.

He’s not married to a product. He’s married to a process. He’s married to this method. This strategy.

If five-year MYGAs return to 6%, he may use those. If index strategies offer better opportunities, he’ll use those.

Dave is:

-

- Adaptable

-

- Disciplined

-

- Intentional

-

- Non-emotional

What This Strategy Is NOT

Let me be clear about something.

This is NOT about saying annuities are always better than bonds.

This is about saying: for bucket one (the first five years of retirement income), Dave wants a defined outcome that isn’t going to fluctuate. He wants a guarantee.

Who Is This Strategy Best For?

This strategy works best for someone who:

-

- Has moderate to high retirement savings

-

- Has diversified assets elsewhere (Dave doesn’t have ALL his money in annuities—that would be ridiculous)

-

- Values certainty over maximum upside

-

- Is comfortable with insurance-backed guarantees

Does Dave have all of his money in annuities? Of course not. But he does have a very sizable chunk of it in annuities using this process.

The Bigger Lesson

Here’s the bigger lesson.

Retirement doesn’t usually fail because of long-term averages.

It fails because of:

-

- Short-term emotional decisions

-

- Not having a strategy with enough guaranteed money

What Dave did was build a system that reduces the need for those emotional decisions.

And honestly, that’s pretty powerful.

Your Next Step

If you could fund the next 5 years in advance, know that one contract is going to mature every year, and remove market volatility for your near-term income—you’d probably feel a lot more confident about your retirement.

This particular strategy isn’t going to work for everybody. But building a customized retirement income strategy that gives you guaranteed income for life? That works for almost everyone.

Whether we do that with a lifetime income rider or we do some sort of bucketing strategy, as Dave has done, depends entirely on your situation.

The best way to find out what strategy would work for you is to book a short Zoom call so we can get your questions answered, and if the opportunity is there, develop a strategy customized to your exact situation.

Episode 103: Retirement Income Strategy To Ladder Annuities For Guaranteed Income

Download Episode 103: Retirement Income Strategy To Ladder Annuities For Guaranteed Income on Apple Podcast