ATLAS ANNUITY RATE REPORT

In this month’s ATLAS Annuity Rate Report, we’ll look at the highest MYGA rates. For the most up-to-date returns or information on FIA’s please click the “Schedule A Call” button.

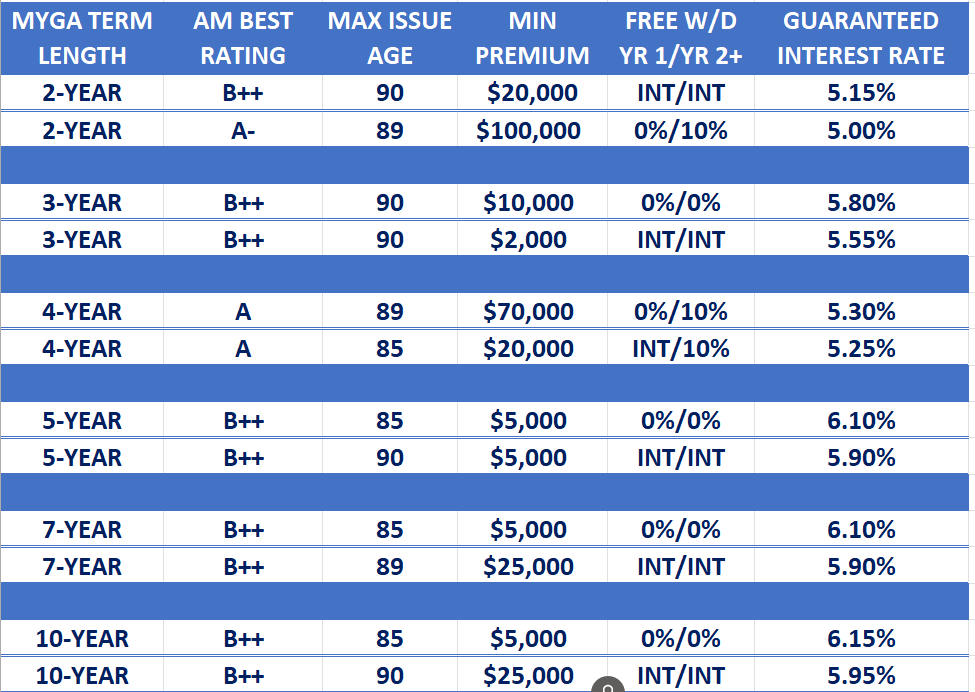

Here are the latest MYGA Rates in the marketplace:

MYGA ANNUITY RATE REPORT

Disclaimer:

Rates shown are for informational purposes only and are based on products available in the State of Missouri as of the date shown. Rates are subject to change at any time, and availability varies by state and carrier. Not all products or rates may be available in all jurisdictions, and this information is not intended as an offer or solicitation.

Atlas Financial Strategies, Inc. works with a select group of insurance carriers based on multiple factors, including financial strength and service considerations. To determine current rates and availability in your state of residence, please contact Atlas Financial Strategies, Inc. directly.

How To Get The Most Out of Annuities:

When we design your ATLAS Annuity Strategy, we will discuss how to use guaranteed income to enhance the safety of your retirement income.

In addition to these phenomenal rates, MYGAs could give you access to 10% of your accumulation value. For a complete strategy on how to effectively use one of these products with my ATLAS Annuity Strategy, instead of bonds or other products that risk your money, all while potentially saving yourself tens of thousands of dollars in management fees, click the link to see a complete overview. Or schedule a time for a short conversation by clicking the “SCHEDULE A CALL” button!

Disclosure:This is a solicitation for insurance based on guaranteed tax-deferred fixed annuity rates. Rates are subject to change. State of residence, age, premium, and financial suitability may determine availability. Early termination surrender charges may apply. Guarantees are backed up by the claims-paying ability of insurance carriers and are not FDIC insured. Certain restrictions and exclusions may apply, which can be found in the contract disclosures. This document is not a legal contract. Martin M. Becker and/or Atlas Financial Strategies, Inc., is an independent insurance agent/agency and does not offer tax or legal advice. This material is for informational or educational purposes only and is not a recommendation to buy, sell, hold, or roll over any asset. It does not consider the specific financial circumstances, investment objectives, risk tolerance, or needs of any specific person. You should work with Martin M. Becker/Atlas Financial Strategies, Inc. to discuss your specific situation.

All the best,

Marty

Your information is secure and will NEVER be shared.

Your information is secure and will NEVER be shared.